„Not so great, Britain!”

10.10.2022

„Not so great, Britain!”

© Feydzhet Shabanov - stock.adobe.com

© Feydzhet Shabanov - stock.adobe.com

Author - Josef Stadler

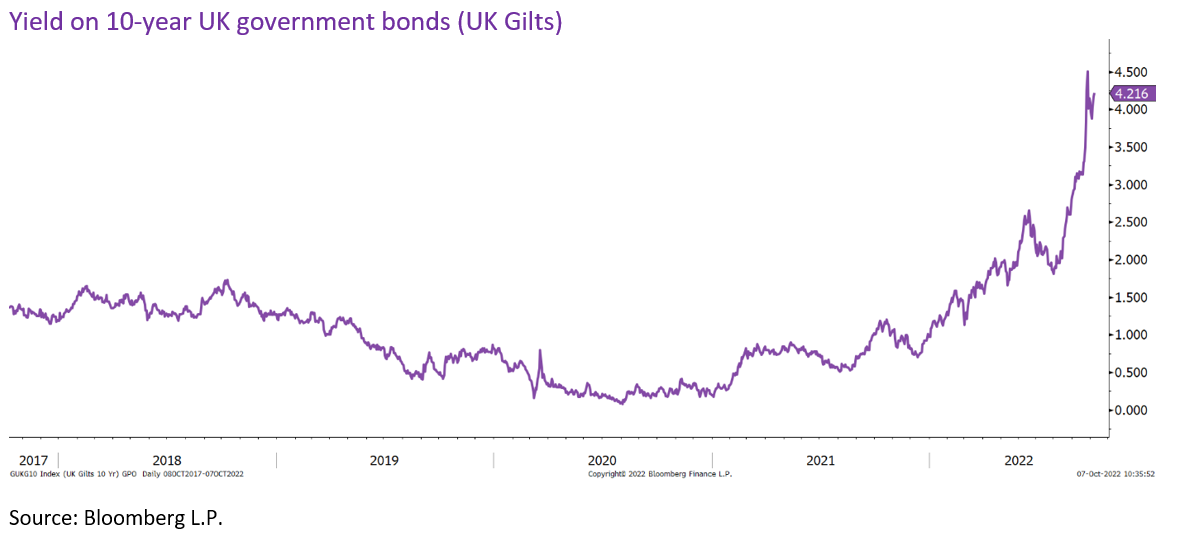

Great Britain is no longer a success story. The immature tax package of neo-prime minister Liz Truss impressively demonstrated how quickly an economy can be plunged into severe turbulences within a short period of time. Yields on British government bonds – the rate at which the government borrows money on the capital markets - rose to as high as 4.50% within hours of the announcement regarding tax cuts by the Chancellor of the Exchequer, additionally the British currency dropped sharply. The Bank of England had to rush out after an "emergency meeting" to contain the chaos unleashed by the new government. “A purchasing of as many government bonds as necessary to restore financial stability will be carried out”, the central bank said. The current situation highlights the impact on the promises made in the 2016 election to leave the EU (“Brexit”). It can now be seen that the promised savings from Brexit have not been realised. It also becomes evident at this point that larger crisis can be better managed in an economic union rather than individually.

Lost glory

The fiscal policy measures also left their mark on the UK stock market. Particularly financial stocks suffered significantly.

The British stock market, once more than a third of the market capitalization in Western Europe, has shrunk to less than a quarter in the last decade. At the end of September 2012, more than 100 British companies were listed in the MSCI Europe Index. By the end of September 2022, that number had fallen to 82. A performance comparison over ten years with the overall index shows a performance that is around 1.5% lower per annum (as total return in euros)! Around 0.95 percentage points of that underperformance can be attributed to the weakening currency rate against the euro.

Despite the current turbulences, the British financial market remains interesting for many investors and companies. This can also be seen by the fact that for example the Dutch consumer goods group Unilever has unified its company structure in favour of the City of London as its headquarter. The energy giant Shell has also relocated its headquarters to England and eliminated the add-on "Royal" from its company name.

As far as the stocks markets overall are concerned, there is a continuing lower weighting on UK equities. The same applies to our Kathrein European Equity equity fund, in which the British stock market was systematically underweighted. Still, there are excellent British companies, with British American Tobacco, Shell and Diageo among the fund's top 10 holdings.

The individual stocks in the fund are selected on the basis of fundamental data, technical indicators and earnings estimates from the world's best analysts. The weighting of the titles is determined using optimization software. We are therefore selectively taking advantage of the opportunities that the UK equity market offers despite the turbulence.

Learn more

Disclaimer:

This marketing communication within the meaning of the German Securities Supervision Act (Wertpapieraufsichtsgesetz) aims to provide a general overview of current market data and does not contain any direct or indirect recommendation for a specific investment strategy in the sense of a financial analysis.

It should be noted that investments in financial instruments entail risks as well as opportunities; value and return may rise, but they may also fall.

The fund currency of the Kathrein European Equity fund is EUR. The management company may enter into transactions with derivatives for Kathrein European Equity as part of the investment strategy. This may at least temporarily increase the risk of loss in relation to assets held in the fund. Derivative instruments that are not used for hedging purposes may be acquired. In this context, investments may also be made predominantly (in relation to the associated risk) in derivatives, whereby the risk amount for market risk (relative VaR) defined for all fund investments at twice the total risk of the reference portfolio must be complied with. Due to the composition of the fund or the management techniques used, the fund exhibits increased volatility, i.e. the unit values are exposed to large upward and downward fluctuations even within short periods of time, and capital losses cannot be ruled out.

The respective valid and published prospectuses, as well as the customer information documents (Key Investor Information - KID) or information pursuant to § 21 AIFMG of the funds managed by Kathrein are available in German free of charge on the website www.kathrein.at and upon request from Kathrein.