The comeback of bonds

19.12.2022

The comeback of bonds

Author - Harald Besser

The painful plunge in bond prices this year was no coincidence and, unfortunately, also to be expected if one looks at the long-term development with negative yields and negative real interest rates in a long-term historical comparison, only the when and how was unfortunately, as so often, not foreseeable. For too long, we have come to terms with ultra-low interest rates and negative yields. So long, in fact, that after a period of astonishment and horror, we have become accustomed to this anomaly. Also, the ever falling yields at longer maturities have been sweetened with juicy price gains.

Return to normality

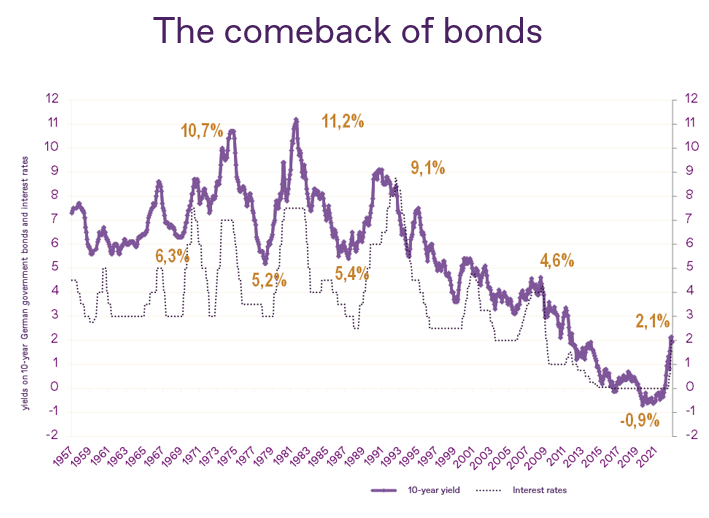

The return to normality had to come sooner or later. After 2022, bonds could now be facing a renaissance. The starting conditions, or current yield levels, are better than they have been for years. Ten-year German government bonds, see chart, currently promise a yield of 2.10% after -0.9% in March 2020. Normally, yields rise with longer maturities, which is then also referred to as a normal yield curve. Currently, this is not the case in Germany or the USA. Inverse yield curves rarely occur and are considered a fairly reliable signal of an impending recession. Interest rates are expected to fall as the economy deteriorates. As a result, shorter maturities, such as two-year German government bonds at 2.4%, generate higher yields than longer maturities. Corporate bonds are somewhat riskier, so we always recommend a portfolio approach here in the form of an ETF or investment fund. Here, yields average around 4%, varying between around 2.5% and 5% depending on the maturity and rating. In the case of high-yield bonds, these are as high as around 8%. Naturally, the risk of default is even higher here, which is why we recommend this category only as an admixture and also only as a portfolio. Bonds from emerging markets countries are also an interesting category to add to a bond portfolio, with a current yield of around 7.4%. If inflation in 2023 does not decline as quickly as assumed, currently around 3.5% inflation is expected at the end of Q1 2024, inflation-linked bonds offer an interesting diversification opportunity.

USD bonds less attractive

In the U.S., interest rates are around 1% to 1.5% higher than in Europe, as the Fed began to tighten its interest rate policy earlier than the ECB. For private investors who invest in euros, however, the addition of USD securities is not worthwhile due to the currency fluctuations.

If you look at the above long-term yield chart of ten-year German government bonds, we have now completed the low-interest phase after the financial crisis. The extent to which interest rates will continue to rise depends to a large extent on the development of inflation in the coming year. Expectations here are quite optimistic, but it will depend on how far the central banks in Europe and on the other side of the Atlantic have to turn the interest rate screw. The inverted yield curve suggests that longer maturities will no longer follow key rates to the full extent, as market participants also already have a slowdown in the economy (from soft landing to deep recession) on their radar next year.

In the bond markets, we are much more optimistic about the new year, hedged by nice yield cushions in all bond classes. We believe the bond markets are ready for a comeback after the painful crash.