Why the Chinese Stock Market Lags Behind Other Emerging Markets

02.06.2026

Why the Chinese Stock Market Lags Behind Other Emerging Markets

Author - Markus Böcklinger

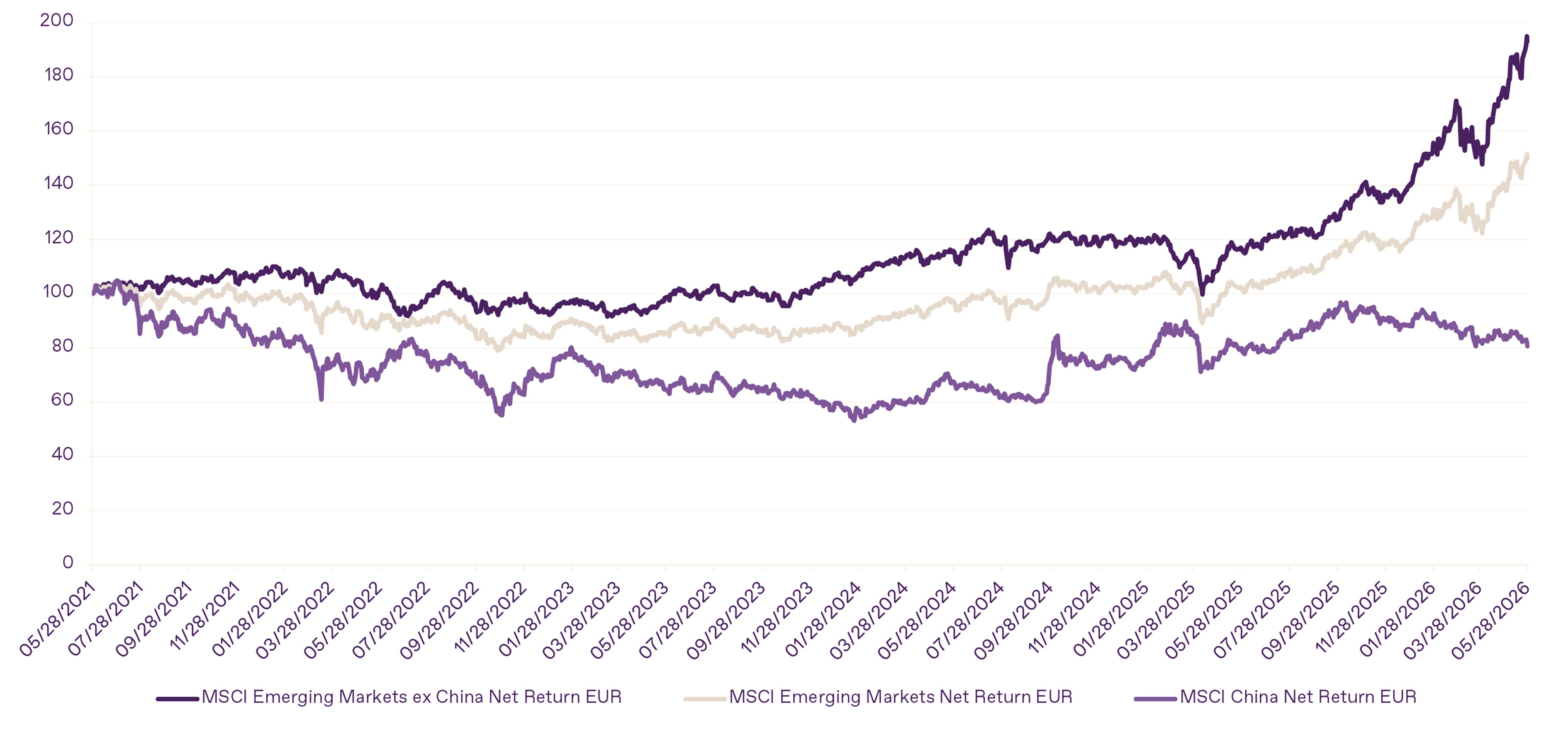

After more than a decade of significant underperformance compared to developed markets, emerging market stock exchanges have shown a noticeable catch-up movement since last year (see chart). This development is mainly driven by the global AI boom, which has sharply increased demand for semiconductors, memory chips, and related infrastructure. Companies from South Korea and Taiwan, as key players in the global chip value chain, have particularly benefited from this trend. Chinese stocks, however, have lagged behind and have so far not been able to participate in the recovery of emerging markets to the same extent. Why is that?

A major reason is the ongoing crisis in the real estate sector, the resulting strain on the banking sector, and the sharply decreased consumer confidence since the strict Zero-Covid policy. As a consequence, domestic demand remained weak, and China’s export dependency increased further. This makes the economy especially vulnerable to new trade policy tensions, which have intensified again since Donald Trump took office. This has led to a ruinous price war in several industries, putting pressure on margins and severely burdening the profit development of many Chinese companies. The resulting deflationary spiral shows parallels to Japan in the 1990s, which is why some observers speak of a “Japanification” of the Chinese economy.

EM Stock Indices Comparison, Bloomberg, May 28, 2026

Politics Before Economy

Additionally, state influence on companies in China is significantly higher than in many other emerging markets. For investors, this means an increased level of uncertainty, as business decisions are not made solely on economic criteria but are often subordinated to political objectives. At the same time, the enforceability of shareholder rights is limited, which can particularly disadvantage foreign minority shareholders.

Moreover, unpredictable regulatory interventions, such as those seen in recent years in technology, education, and gaming sectors, are especially burdensome. The political priority of concepts like “Common Prosperity” shows that social and strategic political goals can take precedence over shareholder interests if necessary. This significantly contributes to Chinese stocks continuing to trade at a structural risk discount.

Risks Outweigh Opportunities

The example of Russian stocks, which became virtually worthless for Western investors after Russia’s invasion of Ukraine, represents an additional risk factor for global investors. It has shown that geopolitical escalations can lead not only to price losses but also to trading suspensions, sanctions, capital controls, or the complete loss of access to invested capital. Against this background, Chinese stocks are viewed with particular sensitivity should political tensions between the US and China escalate further.

In the Kathrein Investment Strategy, we have not invested in Chinese stocks since April 2022.

Disclaimer

This is a marketing communication by Kathrein Privatbank Aktiengesellschaft in accordance with the Securities Supervision Act 2018 and is for informational purposes only. This information aims to provide a general overview of current market data and Kathrein’s market opinion and does not constitute a direct or indirect recommendation for any specific investment strategy in the sense of financial analysis. Investments in securities are subject to price fluctuations due to market changes at any time. Information and representations referring to the past do not allow reliable conclusions about future results. Despite careful research and recording, no liability or guarantee can be assumed for the accuracy of the data.