New All-time-highs – but only across the Atlantic

24.09.2025

New All-time-highs – but only across the Atlantic

Author - Florian König

As expected, the US Federal Reserve cut interest rates by 0.25 percentage points. The key interest rate now ranges from 4.00% to 4.25%. With the prospect of two further cuts at Fed meetings later in the year, US stock markets in particular felt increasing tailwinds. The obvious weakness of the US labor market is also likely to have led to a rethink among voting Fed members, resulting in the first interest rate cut of the year.

Anything but a weakening labor market

Fed Chairman Jerome Powell confirmed this assessment in his speech following the interest rate decision.

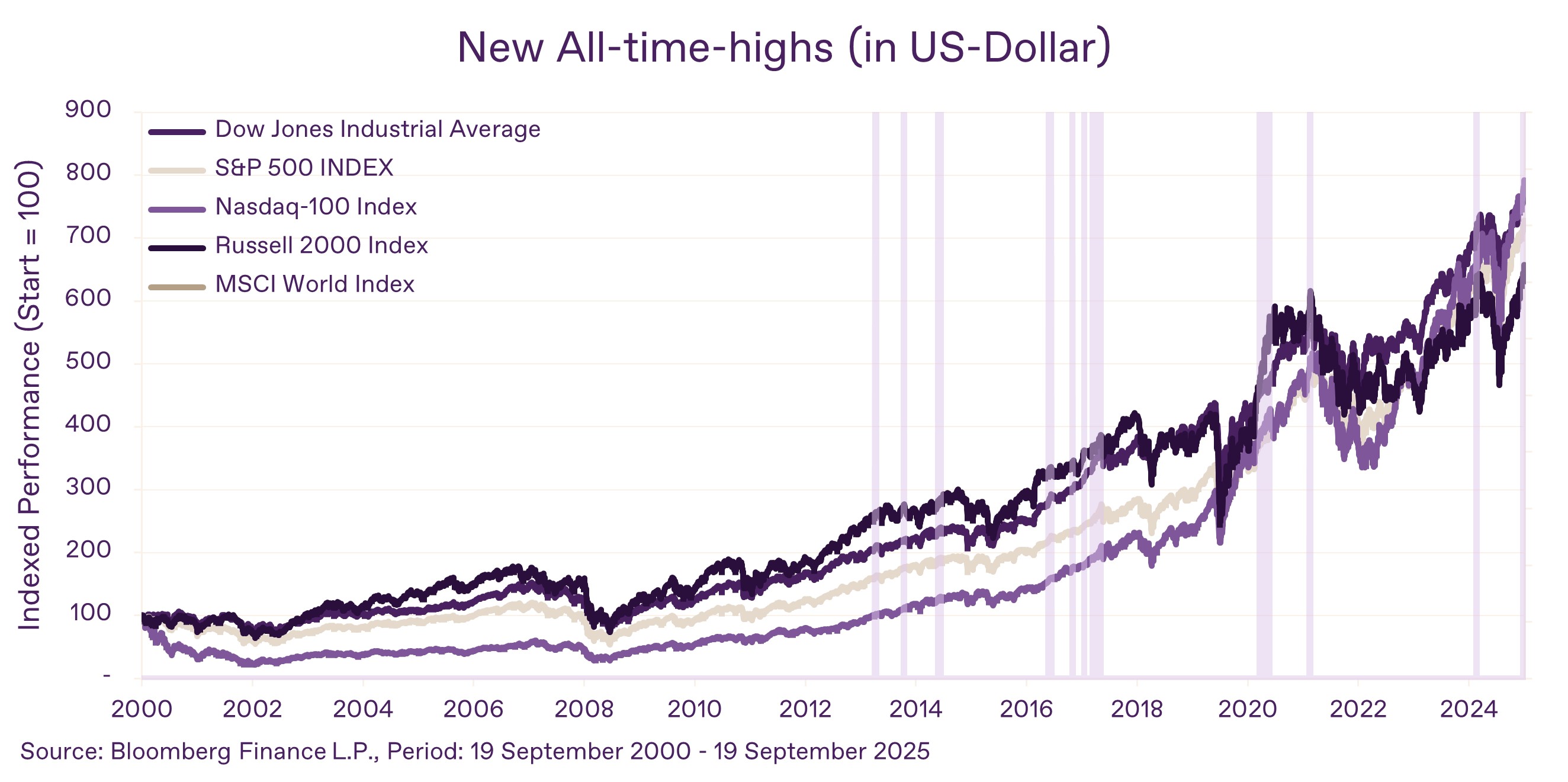

The aim is to avoid rising unemployment figures, a decline in demand and the resulting negative consequences. Although the weakening labor market is a legitimate cause for concern, this aspect did not put an end to the euphoria on the stock markets – on the contrary: the tech rally reached new heights. Driven in part by idiosyncratic (company-specific) news – such as Oracle's positive outlook, takeover intentions for TikTok's US business by US tech companies (including Oracle) and NVIDIA's involvement with Intel – and by the prospect of increasingly loose monetary policy, US indices continued to rise. The result: new highs were reached once again. It is rare for the most important US indices such as the S&P 500, Dow Jones, NASDAQ, and Russell 2000, as well as global indices such as the MSCI World Index in USD, to reach new highs almost in lockstep and continuously. Since the turn of the century, this has only happened 34 times (see vertical indicators in the chart below). This circumstance makes euro investors look enviously across the Atlantic, as these milestones can primarily be claimed by US dollar investors.

Chart: In lockstep to new highs (in US dollars)

When investing in securities, price fluctuations due to market changes are possible at any time. Information and performance data relating to the past do not allow reliable conclusions to be drawn about future results.

What new highs?

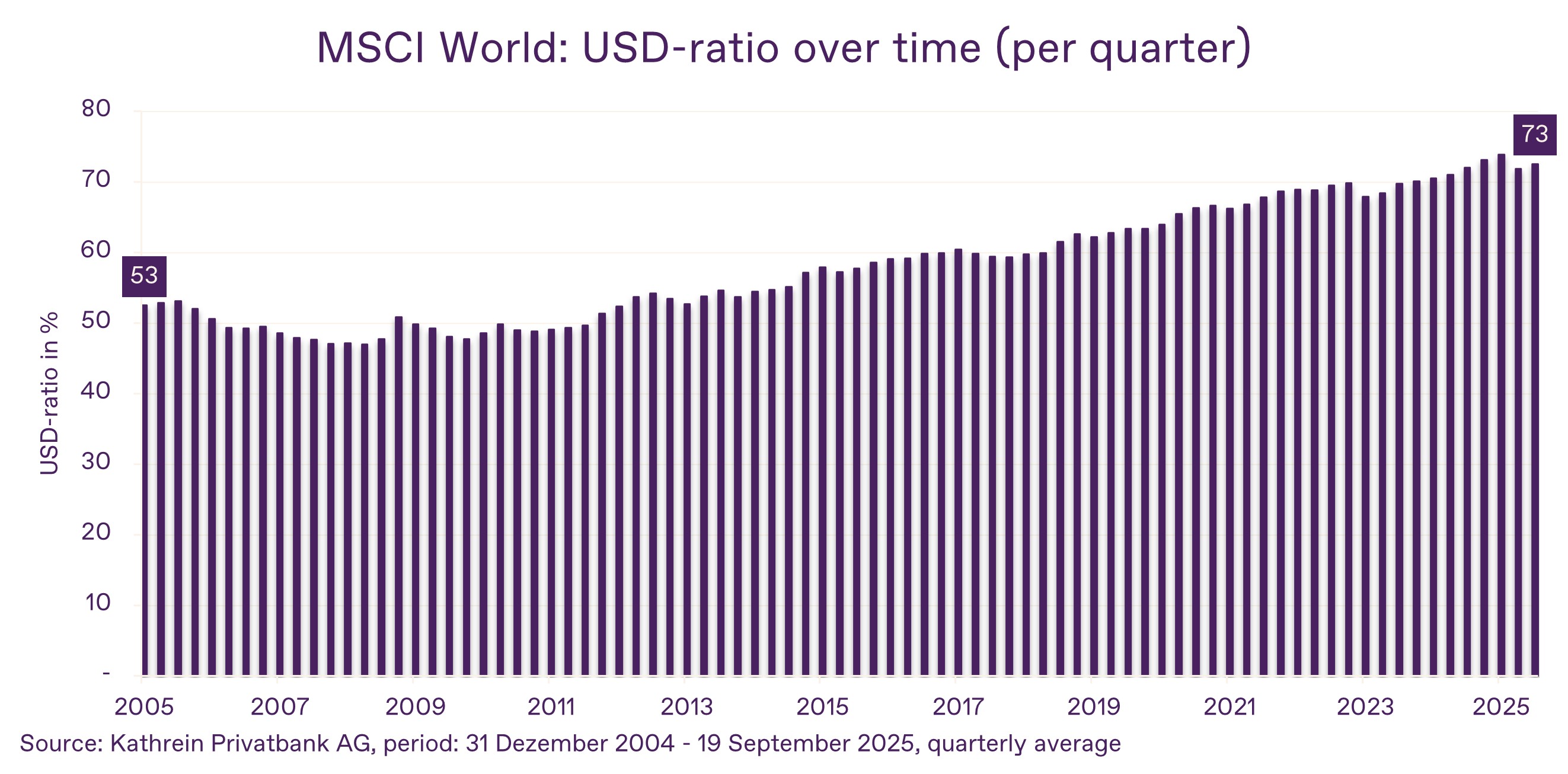

From the perspective of euro investors, the MSCI World (Net Total Return) needs to gain a good 1.7% to reach the high of February 2025. The biggest obstacle to achieving this ambitious goal is the US dollar. Due to its continued weakness, the MSCI World (Net Total Return) EUR Index has recorded a “meager” gain of around 3.0% in the current year (period: December 31, 2024 – September 19, 2025; in the period from September 19, 2020 to September 19, 2025, the index rose by 97.13% Source: Bloomberg Finance L.P.), while the MSCI World (Net Total Return) USD Index gained over 17% in the same period (Source: Bloomberg Finance L.P.). This clearly illustrates the importance of managing foreign currency risks and, in particular, actively managing US dollar risk. One reason for this is that the proportion of stocks listed in US dollars in global indices such as the MSCI World is already around 70%, making it hugely important for future performance from the perspective of euro investors.

Chart: Proportion of companies listed in US dollars in the MSCI World

When investing in securities, price fluctuations due to market changes are possible at any time. Information and performance data relating to the past do not allow reliable conclusions to be drawn about future results.

The increasing concentration of global market capitalization on US tech giants is also strengthening the US dollar's share in global benchmark indices. Active currency exposure is therefore required. Taking the MSCI World as an example: with 100% hedging of foreign currency risk, the gain from the perspective of the euro investor would have already increased to more than 12.9% (period: December 31, 2024 – September 19, 2025; source: Bloomberg Finance L.P.). We therefore rely on an efficient, systematic, and emotion-free approach in the Kathrein Strategy. Strategically, we aim for a hedging ratio of 50% of the US dollar risk, i.e., those stocks that are listed in US dollars, in the equity portfolio. Based on tactical models (including trend following and purchasing power parity), we increase or reduce the hedge depending on our assessment. This can be done by shifting into hedged investment products or derivatives, depending on the orientation of the investment strategy and the permissible financial products. Most recently, the hedge ratio was raised to 62.5%.

Self-awareness is the first step toward possible improvement

Of course, many things seem smarter in hindsight. However, if you don't want to be caught off guard by unfavorable foreign currency movements, you should take a close look at the foreign currency portion of your investments—whether they are one-time investments, ongoing savings plans, or existing investments. Currency movements may balance out in the long term, but interim, potentially painful declines due to currency devaluations, as seen this year, must remain emotionally and financially bearable.

Update on our Kathrein investment strategy

Our Kathrein investment strategy continues to focus on overweighting equities over bonds. The key points can be summarized as follows:

- Interest rates: In view of current developments, we continue to see scope for a further interest rate cut by the Federal Reserve before the end of the year; The development of US inflation is being closely monitored, as the inflation rate remains well above the 2% target. Possible effects of a tightening of US tariff policy are considered to be temporary; on the other hand, greater importance is being attached to the weakness of the labor market in order to prevent a decline in demand from US consumers.

- • US dollar: We have recently increased our hedging ratio from our previous neutral level of 50% of the US dollar share in the equity portfolio to 62.5%. In the bond portfolio, 85% of the US dollar risk continues to be hedged as a result of our optimization. A narrowing interest rate differential between the US dollar and major currencies such as the euro could favor further depreciation of the US dollar.

- • Equities: Within our equity portfolio, we remain underweight in tech giants compared to developed equity markets. Although the strong performance of recent years is based on solid sales and earnings growth, current valuation levels should be viewed with caution; they do not necessarily justify the continuation of high growth rates. Geopolitical conflicts in particular can quickly put an end to growth fantasies if the companies affected find themselves caught between the fronts.

Disclaimer

This information represents a market overview and Kathrein's investment strategy based on its market opinion. It does not contain any direct or indirect recommendation to buy or sell securities or any investment strategy.

When investing in securities, price fluctuations due to market changes are possible at any time. Information and presentations of past performance do not allow reliable conclusions to be drawn about future results. Despite careful research and recording, no liability or guarantee can be assumed for the accuracy of the data.