Why emerging market local currency bonds are attractive at the moment

26.09.2022

Why emerging market local currency bonds are attractive at the moment

Author - Florian König

While rising yields dominate market activity in the developed markets due to rising inflation expectations and the associated tighter monetary policy, emerging market government bonds are outperforming in this calendar year. The reasons for this are as diverse as the investment opportunities in this area.

Anticipation of a tighter monetary policy on the part of the US Federal Reserve

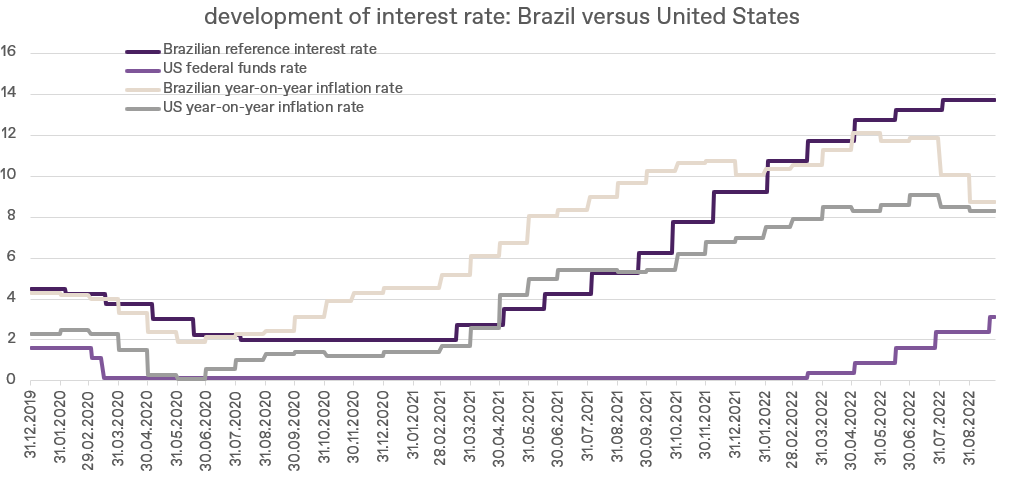

Supply chain issues and resource scarcity, which have been with us for about two years, led to an earlier rethink of monetary policy in emerging markets (see chart). Anticipating the upcoming interest rate cycle in the United States, national central banks felt compelled to implement a tighter monetary policy earlier in order to maintain the attractiveness of their own currency against the US dollar. In the past calendar year, this resulted in a noticeable minus in the price development of the government bond segment.

This year, on the other hand, it proved to be an advantage for many of the emerging markets, as their economies felt the effects of the Ukraine war much less strongly.

Perpetual political risks

What should not be ignored, however, is that all that glitters is not gold. The Achilles' heel of emerging markets is simply the political risk inherent in the individual markets, be it the fast-moving and often difficult political environment, the lack of independence of the central bank or authoritarian aspects in the respective national government. These aspects go hand in hand with incalculable risks and can lead to painful losses on the capital market as soon as capital flows develop to the disadvantage of individual countries. A careful and diversified selection is therefore necessary.

Diversification

In order to be prepared for the risk of negative country-specific events, the focus of emerging market bonds is on diversification. A broad mix of local currencies with a fundamentally positive outlook should be selected in order to reduce cluster risks. Combined with attractive yield expectations and good prospects for the respective local currency, this asset class offers an attractive portfolio component. In addition to sufficient liquidity, the existence of a functioning financial system and the protection of investor interests, an attractive valuation level of the respective national currency should prevail. Here, we are guided by relative purchasing power parity. In addition to financial and economic risks, sustainable assessment is also taken into account. This is where supranational institutions come into play.

Focus on sustainability and credit quality

In order to address the environmental, social and governance weaknesses that often exist in emerging markets, the investment universe can be reduced to a solid basis by taking into account sustainable negative and positive criteria. The breadth of reform needs, whether due to weaknesses in child labour, the death penalty or freedom of speech or press, disqualify many issuers. However, in order to continue to have access to a broad set of issuers and investment opportunities, supranational institutions, such as development banks, offer an opportunity. This reveals another advantage: credit quality. In contrast to government bonds from emerging markets, supranational issuers often have a very good credit rating.

Outlook

In recent months, the emerging market government bond segment has continued to perform well. Even last week, which was once again marked by rising yields in developed markets, further boosted by the UK's fiscal policy plans, emerging market bonds were able to post a gain. This was primarily due to the strength of local currencies.

In the Kathrein Investment Strategy, the sub-asset class "emerging market bonds" continues to be given high importance. Most recently, the share of emerging market bonds within the bond allocation was increased to 15%; a plus of four percentage points. A continuing tighter monetary policy of the US Federal Reserve poses a risk for emerging markets. For as soon as US Treasury yields reach too attractive a level and foreign debt, often US dollar issuance, becomes too expensive, financial market participants could again lean more towards safe havens. This is especially the case if yields in the developed countries return to more attractive levels. However, since any rise in yields is also associated with price declines, such a capital movement is only attractive when the cycle of rising interest rates in the industrialised countries is over - and we do not consider this to be the case yet from today's perspective.