Change of heart on the bond market?

20.02.2023

Change of heart on the bond market?

Author - Thomas ODEHNAL

After the bond market had a spectacular start in January following a year of significant losses in 2022, market participants seem to have come to the conclusion in recent days that the cycle of interest rate hikes could last longer than previously expected. Nevertheless, bonds are now at a quite attractive level due to the increased yields over the last twelve months. Short-term periods of weakness, such as what we are currently seeing, are possible and it is unclear whether this will continue for a while longer. To counter this risk, we have continued to hedge the interest rate risk of the bonds.Nevertheless, bonds are now at a quite attractive level due to the increased yields over the last twelve months. Short-term periods of weakness, such as what we are currently seeing, are possible and it is unclear whether this will continue for a while longer. To counter this risk, we have continued to hedge the interest rate risk of the bonds.

Central bank members on both sides of the Atlantic have been warning since December not to underestimate their willingness to act, but in mid-January, only a few rate hikes were priced in for the period after February, and in the US, bets were already on the first-rate cuts in the current year. In the meantime, however, many market participants are likely to have recognized that the central banks have a pretty good environment to achieve their main goal - maintaining price stability - and to continue raising interest rates.

On the one hand, inflation figures, especially core inflation, which excludes volatile segments of energy and food, continue to be at a high level. On the other hand, the economy is still doing quite well and, at least for now, the risk of a stronger recession seems to have been averted. In addition, labour market data show that capacity utilization remains high, demand exceeds supply in many industries, and thus wage pressure will remain high. Without thinking of the wage-price spiral in the US in the 1970s, this is of course also a driver of higher prices and thus an amplification of inflation.

To curb this inflation, which in Europe is at least four times above the central bank's inflation target, and to bring it down to the targeted two percent in the long term, central banks are likely to take further steps and push the interest rate peak further up and further back than what was traded by market participants in the first weeks of January. A rate hike of 50 basis points to three percent at the March meeting of the ECB seems relatively certain, but whether the rate hike sequence thereafter will really be reduced is not yet a done deal. Similarly, it can also be assumed that a rate hike in March will not be the last for the US Fed this year, and that further hikes will follow.

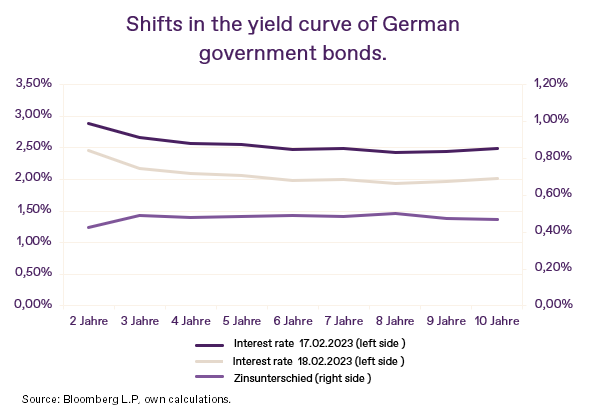

This change of mind has led to a shift in the yield curve at the three-year segment by about 50 basis points since mid-January this year, resulting in corresponding declines in bond prices. The two-year German government bond is now at its highest level in this cycle, at just under 2.9%, while the ten-year bond is close to its year-end high of just over 2.5%.

In recent weeks, some traders may have remembered the good old motto "Never fight the Fed" and it remains to be seen where the interest rate journey will take us this year - because it would be a big surprise if inflation were to fall back to the levels desired by central banks anytime soon.

Thus, hedging against interest rate risk in our portfolios has paid off in recent weeks, as the yield spike was well cushioned.

Disclaimer:

This information represents the market opinion of Kathrein and does not include any direct or indirect recommendation to buy or sell securities or an investment strategy.

When investing in securities, price fluctuations due to market changes are possible at any time. Representations of past performance do not guarantee reliable conclusions about future results.